Four Significant Issues You Need to Consider When Selling Your Business

The process of selling a business can be very complex. Whether you’ve sold a business in the past or are selling a business for the very first time, it is imperative that you work with an expert. A seasoned business broker can help you navigate through what can be some pretty rough waters. Let’s take a closer look at four issues any seller needs to keep in mind why selling a business.

Number One – Overreaching

If you are both simultaneously the founder, owner and operator of a business, then there is a good chance that you are involved in every single decision. And that can be a significant mistake. Business owners typically want to be involved in every aspect of selling their business, but handling the sale of your business while operating can lead to problems or even disaster.

The bottom line is that you can’t handle it all. You’ll need to delegate the day-to-day operation of your business to a sales manager. Additionally, you’ll want to consider bringing on an experienced business broker to assist with the sale of your business. Simultaneously, running a business and trying to sell has gone awry for even the most seasoned multitaskers.

Number Two – Money Related Issues

It is quite common that once a seller has decided on a price, he or she has trouble settling for anything less. The emotional ties that business owners have to their businesses are understandable, but they can also be irrational and serve as an impediment to a sale. A business broker is an essential intermediary that can keep deals on track and emotions at a minimum.

Number Three – Time

When you are selling a business, the last thing you want is to waste time. Working with a business broker ensures that you avoid “window shoppers” and instead only deal with real, vetted prospects who are serious about buying. Your time is precious, and most sellers are unaware of just how much time selling a business can entail.

Number Four – Don’t Forget the Stockholders

Stockholders simply must be included in the process whatever their shares may be. A business owner needs to obtain the approval of stock holders. Two of the best ways to achieve this is to get an attractive sales price and secondly, to achieve the best terms possible. Once again, a business broker serves as an invaluable ally in both regards.

Selling a business isn’t just complicated; it can also be stressful, confusing and overwhelming. This is especially true if you have never sold a business before. Business brokers “know the ropes” and they know what it takes to both get a deal on the table and then push that deal to the finish line.

When Selling Your Business, Play to Win

If you are an independent business owner, you are most likely also an independent business seller–if not now, you will be somewhere down the road. The Small Business Administration reports that three to five years is a long enough stretch for many business owners and that one in every three plans to sell, many of them right from the outset. With fewer cases of a business being passed on to future generations, selling has become a fact of independent business life. No matter at what stage your own business life may be, prepare now to stay ahead in the selling game.

Table of Contents:

Perhaps one of the most important rules of the selling game is learning how not to “sell.” An apt anecdote from Cary Reich’s The Life of Nelson Rockefeller shows a pro at work doing (or not doing) just that:

When the indomitable J.P. Morgan was seeking the Rockefeller’s Mesabi iron ore properties to complete his assemblage of what was to become U.S. Steel, it was Junior [John D. Rockefeller, Jr.] who went head-to-head with the financier. “Well, what’s your price?” Morgan demanded, to which Junior coolly replied, “I think there must be some mistake. I did not come here to sell. I understand you wished to buy.” Morgan ended up with the properties, but at a steep cost.

As this anecdote shows, the best approach to succeeding at the selling game is to be less of a “seller” and more of a “player.” Take a look at these tips for keeping the score in your favor:

Let Others Do the Heavy Pitching

Selling a business is an intense emotional drain; at best, a distraction. Let professional advisors do the yeoman’s duty when selling a business. A business intermediary represents the seller and is experienced in completing the transaction in a timely manner and at a price and terms acceptable to the seller. Your business broker will also present and assess offers, and help in structuring the transaction itself. If you plan to use an attorney, engage one who is seasoned in the business selling process. A former Harvard Business Review associate editor once said, “Inexperienced lawyers are often reluctant to advise their clients to take any risks, whereas lawyers who have been through such negotiations a few times know what’s reasonable.”

Stay in the Game

With the right advisors on your side, you can do the all-important work of tending to the daily life of the business. There is a tendency for sellers to let things slip once the business is officially for sale. Keeping normal operating hours, maintaining inventory at constant levels, and attention to the appearance and general good repair of the premises are ways to make the right impression on prospective buyers. Most important of all, tending to the daily running of the business will help ward off deterioration of sales and earnings.

Keep Pricing and Evaluation in the Ballpark

Like all sellers, you will want the best possible price for your business. You have probably spent years building it and have dreamed about its worth, based on your “sweat equity.” You’ll need to keep in mind that the marketplace will determine the value of the business. Ignoring that standard by asking too high a price will drive prospective buyers away, or will at the least slow the process, and perhaps to a standstill.

Play Fair with Confidentiality

Your business broker will constantly stress confidentiality to the prospects to whom he or she shows your business. They will use nonspecific descriptions of the business, require signatures on strict confidentiality agreements, screen all prospects, and sometimes phase the release of information to match the growing evidence of buyer sincerity. As the seller you must also maintain confidentiality in your day-to-day business activities, never forgetting that a breach of confidentiality can wreck the deal.

Sell Before Striking Out

Don’t wait until you are forced to sell for any reason, whether financial or personal. Instead of selling impulsively, you should plan ahead carefully by cleaning up the balance sheet, settling any litigation, providing a list of loans against the business with amounts and payment schedule, tackling any environmental problems, and by gathering in one place all pertinent paperwork, such as franchise agreement (if applicable), the lease and any lease-related documents, and an approximation of inventory on-hand. In addition, you could increase the value of your business by up to 20 percent by providing audited financial statements for one or two years in advance of selling.

Think Twice Before Retiring Your “Number”

The trend is for sellers to assume they will retire after selling the business. But consider this: agreeing to stay on in some capacity can actually help you get a better price for your business. Many buyers will pay more to have the seller stay aboard, thus helping to reduce their risk.

Keep the Ball Rolling

You need to keep the negotiation ball rolling once an offer has been presented. Even if you don’t get your asking price, the offer may have other points that will offset that disappointment, such as higher payments or interest, a consulting agreement, more cash than you anticipated, or a buyer who seems “just right.” The right buyer may be better than a higher price, especially if there is seller financing involved, and there usually is. In many cases, the structure of the deal is more important than the price. And when the ball is rolling, allow it to pick up speed. Deals that drag are too often deals that fail to close.

By following these tips, and by working closely with your business broker, you can have confidence in being a seller who, like John D. Rockefeller, Jr., doesn’t “come here to sell.” You will play the selling game–and be a winner.

Understanding Issues Your Buyer May Face

Not every prospective buyer buys a business. In fact, out of 15 prospective buyers, only 1 makes a purchase. Sellers should remember that being a buyer can be stressful. The bottom line is that buying a business is usually one of the single largest financial decisions that a person can make. In this article, we are going to explore a few of the reasons why being a buyer can be both stressful and taxing. Keeping a buyer’s perspective in mind will help you on the road to successfully selling your business.

A prospective buyer has many decisions to make before he or she decides to buy a business. Many prospective buyers are employed, and that means they will have to leave their existing jobs to buy a business. Simply stated, a buyer will have to leave the safety and security of their job and “strike out on their own.”

There are also other substantial financial concerns for buyers as well. The majority of buyers will have to take out loans to purchase a business. Additionally, the new owner will need to execute a lease or assume the existing list. At the end of the day, there exists an array of weighty business decisions that a buyer must make.

Ultimately, a buyer has to decide whether or not he or she is ready to take a giant step and purchase a business. This is more than just a financial decision. The enormity of the decision to purchase a business is such that touches every aspect of a person’s life. Owning a business can be very time-consuming and demand a great deal of one’s attention. The result is that buying a business has a direct impact on both one’s financial life and one’s personal life. Owning a business can be extremely time-consuming and this is particularly true for new business owners.

Prospective buyers need to weigh all the factors involved in buying a business. Caution must be exercised. Buyers need to step back and fully assess whether or not owning a business is right for them both on a personal and financial level. When sellers put themselves in their buyer’s “shoes,” things begin to look a bit differently.

When it comes to buying or selling a business, the assistance of a business broker is invaluable. A business broker understands what is involved in owning a business and can help both buyers and sellers evaluate the pros and cons of any transaction.

Copyright: Business Brokerage Press, Inc.

Read More

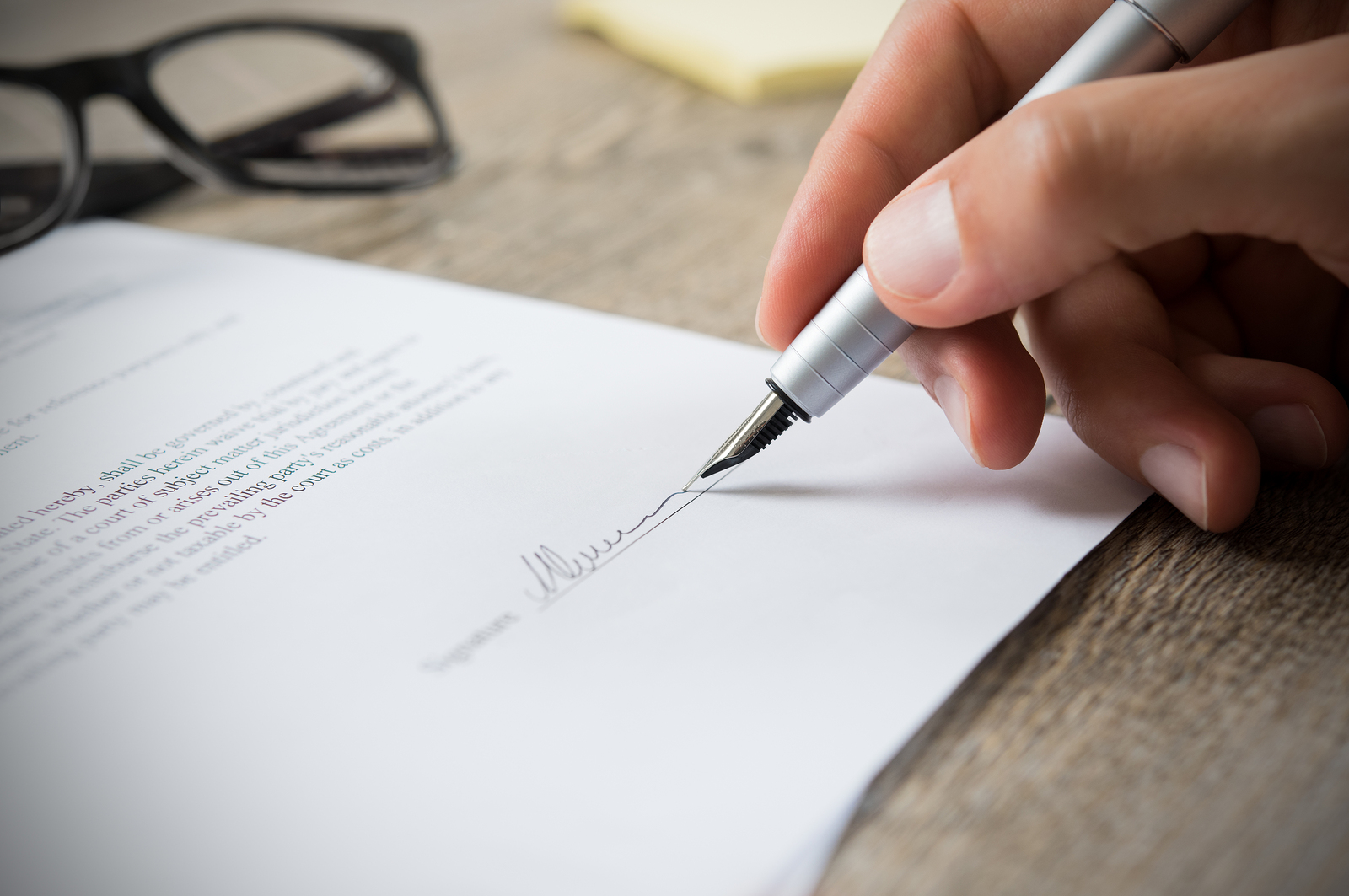

Avoiding Legal Mistakes When Selling Your Business

A common mistake that many make when preparing to buy or sell a business is to overlook all the various legal issues involved. A legal mistake can bring the entire process to a screeching halt or even worse case cost you a small fortune. For this reason, it is important to carefully evaluate the full slate of relevant legalities. This article will explore some of the key legal points one need to consider long before placing your business on the market.

Mistake #1 Neglecting to Have a Non-Disclosue Agreement

Having potential buyers sign a Non-Disclosure Agreement, or NDA, is critically important when selling your business. One benefit to having this agreement signed and sealed is that in the event that the deal falls through, which often happens, the buyer can’t disclose the details to other parties. However, if you don’t have an NDA, the buyer could reveal important aspects of your discussions. This could impact any future sales.

Mistake #2 Failing to Get an Experienced Attorney

There are times to cut corners, and then there are times when cutting corners or trying to save a dollar is a big mistake. Prepping to sell your business is one of those occasions where investing in good and proven counsel is a must. A good attorney can give you a range of legal moves you should and should not make.

Additionally, hiring an attorney with an established experience is just what you need to create ironclad agreements. Sellers have an array of risks that they must face when selling a business. For example, the seller needs protection from a potential buyer hiring away key employees. Without ironclad agreements and a tight NDA, a buyer could pass on buying the business, yet “steal” employees or weaken business in other ways.

Mistake #3 Skipping the Letter of Intent

Another legal way to protect your interests comes in the form of a letter of intent. This letter should be one of your key tools in negotiating the deal. Included in this letter should be a termination fee for the buyer. This applies in the event that the buyer walks away for a reason that is not the seller’s fault. Inclusion of this clause means that the seller is far less impacted if the deal does not go through as planned. Further, this clause goes a long way in ensuring that only serious buyers are attracted.

Reap the Benefits of Ample Preparation

These are just a few of the many errors that sellers often make and regret later on. It is a worthwhile investment to take the legal aspects of selling your business seriously. If you prepare for the sale of your business, you will have a much more successful experience. That means you should work with a proven and competent attorney and business broker before you put your business on the market.

Copyright: Business Brokerage Press, Inc.

Read MoreWhen Selling Your Business: Confidentiality Is Key

You’ve make the big decision to sell. Your books are in order, you’ve spiffed up the premises. What are you waiting for?

Many sellers get to this threshold and then become concerned about confidentiality. They do not want the news of their decision to reach their customers, competitors, employees, or creditors. After all, they figure, customers may lose confidence in the business and go elsewhere, competitors might use this opportunity to spread rumors, employees might fear for their future security, and creditors might push for earlier payment. Not all of these qualms are reasonable; however, when selling a business, discretion is definitely the better part of valor. Few, if any, transactions have been wrecked due to excessive discretion. A breach of confidentiality, on the other hand, can severely alter the course of the transaction. What can you do to protect yourself against this possible deal-wrecker?

Table of Contents:

- Qualify the Buyer

- Use Appropriate Marketing Strategies

- Prepare Paperwork Designed to Promote Confidentiality

- Manage Appropriate Release of Information

Your first step is to look for expert guidance. When a business broker is involved in the sale, he or she will channel the process to keep the transaction within safely silent bounds. You can expect your business intermediary to do the following:

1. Qualify the Buyer

Screening potential buyers is one of the most important benefits a business broker can provide for you. Keep in mind that roughly 90 percent of those who respond to business-for-sale ads are either not serious buyers or are not financially qualified. By screening prospects, the business broker will contribute to confidentiality by limiting the exposure of the business to the most promising buyers instead of to the merely curious time-wasters.

2. Use Appropriate Marketing Strategies

How can you advertise a business for sale without spreading the news too far? The business broker, as intermediary, is in an ideal position to do just that. Brokers place advertising and post listings that contain non-specific descriptions of the business. This “blind ad” approach can be phrased to attract interest in the business without revealing its name or exact location.

30 Prepare Paperwork Designed to Promote Confidentiality

After screening prospective buyers and assessing the degree of interest and financial qualification, the business broker will also require prospects to sign a strictly worded confidentiality agreement.

4. Manage Appropriate Release of Information

Until a purchase-and-sale agreement has been signed, the business broker can phase the release of information about the business to match the growing evidence of buyer sincerity and trustworthiness.

However, even with the most careful handling, rumors are unavoidable. The wise seller will expect questions from the curious and will be ready with answers. If you find yourself needing to muffle the business-for-sale buzz, aim for a mix of good sense and good humor. You might respond that many buyers have approached you over the years, making “news” before it happens. You could go on to say that you never refuse to listen to a great offer, adding that you are, in fact, all ears right at that moment!

No matter how close-mouthed sellers choose to be with the community at large, they might consider being open with their own employees. This is the group most likely to sense what’s happening, and sharing the news with workers can sometimes be a positive move. Since it’s often the unknown that causes the most anxiety, including employees in the decision to sell can actually calm over-active imaginations. Once enlightened, workers can be made to understand the need for discretion. Confidentiality will help protect their own future as well as that of the business.

What Every Seller Should Know

Selling your business is a major decision! You have devoted your time, money and energy to building, running and operating your business. It may well represent your life’s work. You have decided that now is the right time to sell, and you want the very best professional guidance you can get. This is when working in tandem with a professional business broker can make the difference between just getting rid of the business and selling it for the very best price and terms. Following are some of the most common questions asked by sellers — and if you are contemplating selling your business, these are questions you should be asking, too.

1. What Can — and Can’t — A Business Broker Do for Me?

Business brokers are the professionals who will facilitate the successful sale of your business. It is important that you understand just what professional business brokers can do — as well as what they can’t. Business brokers can help you decide how to price your business and how to structure the sale so it makes sense for you and the buyer. They can find the right buyer for your business, work with the seller and the buyer in negotiating, and coordinate every step of the way until the transaction is successfully closed. They will also help the buyer with all details of the business buying process.

A business broker is not, however, a magician who can sell an overpriced business. Most businesses are salable if priced and structured properly. You should understand that only the marketplace can determine what a business will sell for. The amount of the down payment you are willing to accept along with the terms of the seller financing can greatly influence not only the ultimate selling price, but the success of the sale itself.

2. Why Is Seller Financing Important To the Sale Of My Business?

Surveys have shown that sellers who ask for cash receive, on average, only 75 percent of their asking price, while sellers who accept terms typically receive 86 percent of their asking price. In many cases, businesses that are listed for all cash just don’t sell. With reasonable terms, however, the chances of selling increase dramatically, and the time period from listing to sale greatly decreases. Most sellers are unaware of how much interest they can generate by financing the sale of their business. What’s more, seller financing tells the buyer that the seller is confident about the ability of the business to — literally — pay for itself.

3. How Long Will It Take To Sell My Business?

It generally takes, on average, between three to four months to sell a business. (Keep in mind, however, that an average is just that.) The sooner the business broker has all the information needed to begin the marketing process, the shorter the time period for selling should be. It is also important that the business be priced properly right from the start. Some sellers, operating under the premise that they can always come down in price, overprice their business, not understanding that buyers often will refuse to look at an overpriced business.

It has been shown that the amount of the down payment may be the key ingredient for a quick sale. The lower the down payment, generally 40 percent of the asking price or less, the shorter the time to a successful sale. A reasonable down payment also — as in the case of seller financing — sends a message to a potential buyer about the seller’s confidence in the health of the business.

4. What Happens When There Is A Buyer For My Business?

When a buyer is sufficiently interested in your business, business brokers will help in the preparation of an offer or proposal, which may have one or more contingencies. Usually, contingencies call for a detailed review of your financial records and may also include a review of your lease arrangements, franchise agreement (if there is one) or other pertinent details of the business. The buyer’s proposal will be presented to you for your consideration. You may accept the terms of the offer or you may make a counter-proposal. You should understand, however, that if you do not accept the buyer’s proposal, the buyer can withdraw it at any time.

Business brokers will submit all offers to you for your consideration. At first review, you may not be pleased with a particular offer: it may be lacking in some areas, but it might also have some pluses to seriously consider. Remember the old adage: The first offer is generally the best one the seller will receive.” This does not mean that you should accept the first, or any offer — just that all offers should be looked at with thought and care.

When you and the buyer are in agreement, the business broker will work with both of you to satisfy and remove the contingencies in the offer. It is important that you cooperate fully in this process; otherwise, the buyer might think you have something to hide. The buyer may, at this point, bring in outside advisors to help them review the information. When all the conditions have been met, final papers will be drawn and signed. Once the closing has been completed, money will be distributed and the new owner will take the possession of the business. Your business broker professional will work with you throughout the entire sales process.

5. Co-Branding: The New Age Business Combo

The store-within-a-store is not a novel concept. The tailor next to the dry cleaner, for example, is a combination that’s been around since the beginning of business time.

Now combining business forces has a new look — and a new name. It’s called co-branding, and the idea is going like hotcakes. Like hotcakes with a side of motor oil. Among franchises, where the concept is most popular, co-branding means selling combined products and/or services at the same place of business. The combinations may sometimes seem unlikely, but any way you slice it, co-branding seems to work.

6. Co-Branding for One-Stop Convenience

This type of co-branding can produce some stomach-churning combos. Fast food and fuel, currently the most popular oddball mix, proves it can be convenience alone that makes the idea work.

For example, it’s lunchtime and you also need gas. Why settle for Nabs and a Coke from the service station machine? Why go to McDonald’s for your fast-food feast and then hit the road again for gas? Instead, while munching on your double-decker Italian at a Subway, your car is being gassed and car windows are being washed. One stop — and two items are off your list.

When the combined franchises are both nationally-recognized big names, each one benefits from the business attracted by the other. And in cases where one member of the combo is better-known, the bigger name draws traffic to the other. There are also real financial advantages when two or more businesses co-brand. They will shoulder equally expenses such as rent, telephone lines, and most utilities.

7. Co-Branding for Synergy

Adding synergy to convenience makes a hard-to-beat selling technique. Business accounting services with a next-door-copy center, an office-supply store with a packing/shipping outfit, the bookshop that houses a coffee bar — when different franchises are placed within one location, each can concentrate on its own special products or services. From the franchisor’s point of view, co-branding increases efficiency and customer satisfaction.

These two-for-one operations bank on the attraction of allied products or services. The key here is to predict customer need — and in the case of the bookshop coffee bar — mood. Having fulfilled his/her original shopping purpose, what might the customer be drawn to next? This leads us to the next type of co-branding …

8. Co-Branding for Impulse Purchase

The best example here is the national fast-food vendor, Arby’s. This company also owns T.J. Cinnamons (breads and muffins). How better to introduce a new food concepts than to put them side-by-side with good old established roast beef? After lunch, go ahead and get your breakfast buns as long as they’re right there.

From the point of view of the companies involved, this doubling-up (or even tripling up) means more than just increased sales. It makes good business sense all the way around. The space isn’t all that’s shared — a wise financial move in itself — but also payroll expenses and, in some cases, the workers themselves. After the breakfast rush, the crew can go next door and help set up for lunch. If one business melds better with the summer season and another with winter, employees can be concentrated to follow customer traffic.

So what’s not to like about co-branding? So far, so good. For franchisors everywhere, it looks like a win-win combination.